FuE Employees Abroad

This funding consultation does not constitute legal advice pursuant to § 3 RDG or assistance in tax matters pursuant to § 1 StBerG. This is only thorough research and not legal advice.

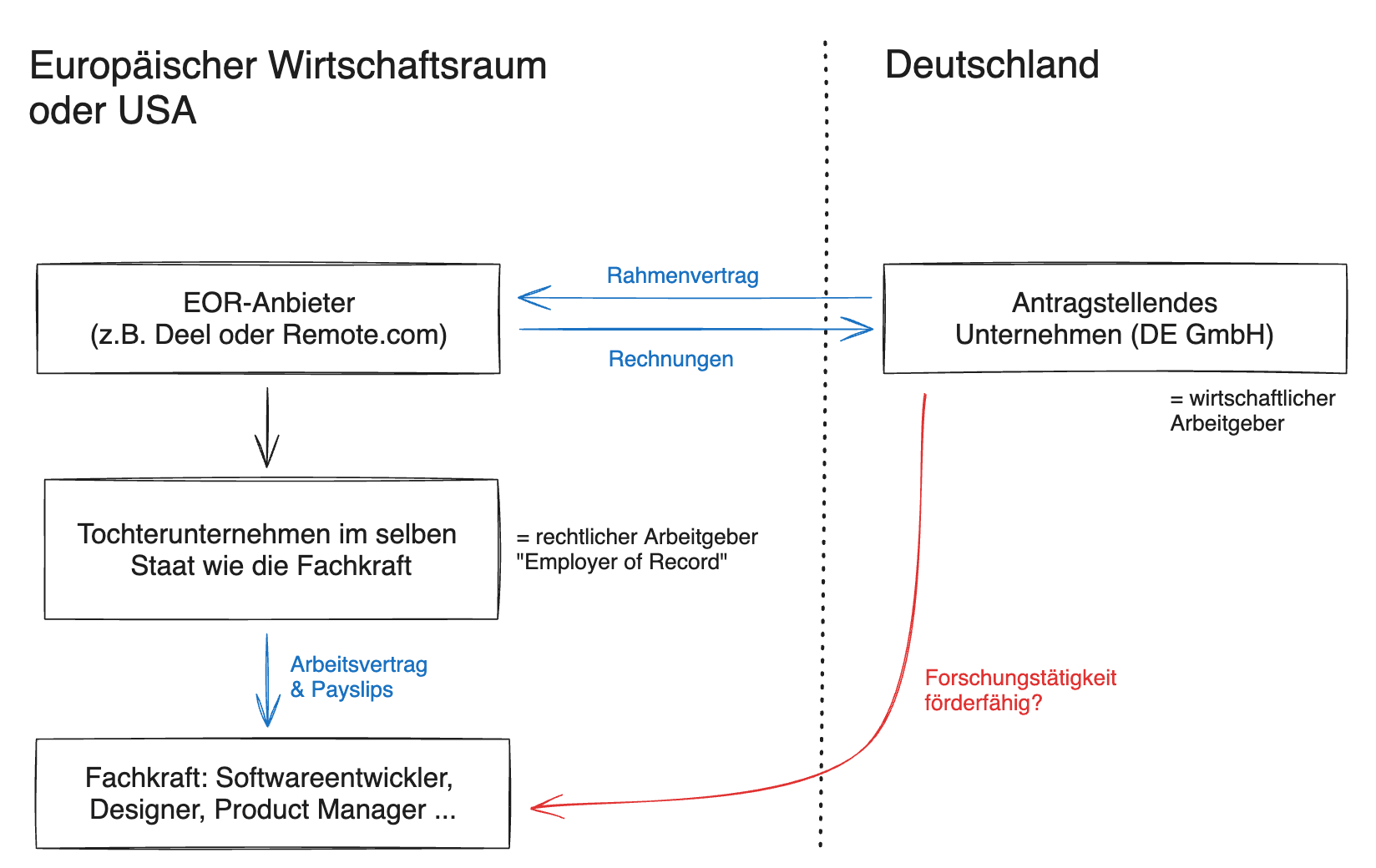

A central question is the extent to which personnel costs for employees working abroad are eligible under the Forschungszulage (FZulG), particularly when modern employment models such as the use of an Employer of Record (EOR) are used.

Basics of Personnel Cost Eligibility under § 3 FZulG

According to § 3 para. 1 and 2 FZulG, eligible expenditures in the context of in-house research and development (FuE) include in particular wages subject to payroll tax as well as the employer's contributions for future security of its employees (§ 3 no. 62 EStG), insofar as these relate to the share of eligible wages.

The decisive criteria here are:

- Payroll tax liability in Germany: As a general rule, only wages for which the employer must withhold payroll tax in Germany are eligible. The company must act as a "domestic employer" within the meaning of payroll tax law.¹

- Directness of payment: The employer must pay the wages directly to the employee for their actual work on FuE activities in an eligible FuE project.¹

- Exception under DBA: Also eligible are those portions of wages for which, under a double taxation agreement (DBA), the right of taxation is assigned to another EU member state, another contracting state of the EWR Agreement, or the Swiss Confederation. The requirement is that the wage would in principle be subject to German payroll tax, but is only exempt due to the DBA. The employee must therefore be employed by the applying German company (German employment relationship).¹

The Challenge: Employees Abroad via an Employer of Record (EOR)

To simplify the process of hiring abroad and to ensure compliance with local legal and tax regulations, many German companies use specialised service providers (so-called Employer of Record – EOR). These act legally as the employer abroad, conclude the employment contract with the employee, pay the salary and remit local taxes and contributions, while the employee effectively works for the German company and is subject to its instructions.

This arrangement leads, under a strict interpretation of the FZulG, to problems with the eligibility of personnel costs:

- Lack of directness: The German company (applicant for the Forschungszulage) does not pay the wages directly to the employee. Payment is made by the EOR as the formal employer. According to the BMF's requirements, wages paid by third parties do not count as eligible wage expenditures.¹

- No own employee: The employee is formally not employed by the applying German company, but by the EOR. The FZulG, however, only takes into account an entitled party's "own employees".¹

- No German payroll tax liability: Since the EOR is based abroad and acts as the employer there, German payroll tax is generally not withheld. Under this reading, the DBA exception also does not apply here, since there is no originally German payroll tax relationship that is merely exempted by a DBA.

Under this strict analysis, salary payments for employees employed abroad via an EOR would not be recognised as the German company's own wage expense, even if the German company reimburses the costs to the EOR via a services agreement.

Alternative View: Economic Substance and Contract Structuring

The following points support this alternative view:

- Economic cost-bearing: If the German company is contractually obligated to the EOR to cover all costs for the employee (salary, supplements, social contributions, etc.) and demonstrably reimburses these (e.g. via invoicing and billing), the German company bears the economic burden of the wages. "Directness" could therefore be considered fulfilled economically.

- Contractual arrangements: The services agreement between the German company and the EOR is decisive. If this contract clearly stipulates that the EOR acts merely as an administrative processor and that the German company bears the full costs for the specific employee and their FuE activities, this could support the economic attribution.

- Attribution under DBA via EOR subsidiary: Even if the EOR has its registered office outside the EU/EWR, eligibility under this argument may exist if the employee is employed via a subsidiary of the EOR that has its registered office in an EU member state or EWR contracting state. The employment contract is then concluded with this local subsidiary. Accordingly, the eligible wages (economically borne by the German company) are attributed to the respective EWR contracting state where the subsidiary has its registered office. The requirement of attribution to an EU/EWR/CH state would thereby be met.

- Eligible wage components: Eligible (and thus potentially fundable) wages subject to payroll tax also include special payments subject to payroll tax deduction, such as annual bonuses, performance allowances, and overtime compensation.³ Similarly, the employer's contributions for future security (§ 3 no. 62 EStG) are eligible insofar as they relate to the eligible wages.⁴

Under this economic analysis, the expenditures for an employee employed abroad via an EOR could qualify as eligible wages, since the German company economically bears the wages and the attribution to an eligible state (via the EOR subsidiary) is established.

Qualification of Employees

Regardless of the form of employment, the following applies: FuE activities are generally carried out by persons who are qualified to perform the necessary FuE work. A particular level of formal qualification is not required.⁵ Qualification is usually uncontested as long as the person actually carries out the FuE tasks.

Conclusion

The eligibility of personnel costs for employees employed abroad via an EOR under the Forschungszulage is legally complex and has not been conclusively resolved.

- The strict, formal interpretation by the tax authorities (based on the BMF letter) considers such costs as not eligible, since the direct payment by the applicant is lacking and there is often no original German payroll tax relationship. This is currently the safest assumption.

- An alternative, economic perspective argues that with appropriate contract structuring that clearly demonstrates economic cost-bearing by the German company, the requirements for eligibility could be met. This depends strongly on the details of the services agreement with the EOR and the willingness of the reviewing authority (Bescheinigungsstelle Forschungszulage – BSFZ / tax office) to follow this line of reasoning.

Companies using EOR models that wish to apply for the Forschungszulage should:

- Review and structure the contracts with the EOR very carefully to clearly document economic cost-bearing.

- Be aware of the legal uncertainty and factor in the risk of non-recognition.

- If appropriate, seek a binding ruling or clarification with the competent authorities.

- Examine as a safer alternative whether a direct employment with the German company with secondment or local employment via the company's own foreign permanent establishment or subsidiary is feasible, in order to clearly fulfil the requirements of the FZulG.

- Examine the option of contract research (§ 3 para. 3 FZulG), although it is questionable whether an EOR would be recognised as a contractor for FuE services, since it does not itself conduct research.

It remains to be seen how practice and potentially case law will develop in relation to this constellation.

Footnotes:

¹ Cf. BMF letter of 7 February 2023, para. 76 ² Cf. BMF letter of 7 February 2023, para. 92 (with reference to § 38 para. 1 sentence 2 EStG) ³ Cf. BMF letter of 7 February 2023, para. 90 ⁴ Cf. BMF letter of 7 February 2023, para. 103